I. Overview

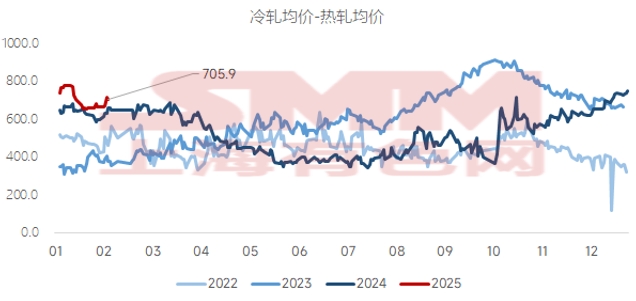

The price trend of cold-rolled coil (CRC) from January-February showed an initial jump followed by a pullback, accompanied by a narrowing price spread between hot-rolled coil (HRC) and CRC, though still fluctuating at highs. The narrowing price spread was mainly due to the fluctuating decline in CRC prices, which actively reduced the price difference. For CRC, in terms of supply, current CRC profits were favorable, and steel mills showed high enthusiasm for CRC production. CRC production from January-February remained at high levels. On the demand side, due to the Chinese New Year holiday and the off-season for consumption, apparent demand for CRC from January-February declined MoM. The strong supply and weak demand pattern led to a rapid inventory buildup of CRC. For HRC, although it also faced a strong supply and weak demand pattern with off-season inventory buildup from January-February, HRC prices fluctuated rangebound overall during January-February, supported by positive macro expectations and strong cost support.

As shown in the chart, the price spread between HRC and CRC jumped initially and then pulled back during January-February, with the spread exceeding 800 yuan/mt before declining. The main reason was that apparent demand for CRC in December 2024 increased by about 5% YoY. To respond to the anticipated tariff policies after Trump's inauguration, home appliance and automotive sectors increased export orders, boosting CRC consumption demand. In terms of supply, although CRC production remained higher than the same period last year, logistics were affected by weather conditions, slowing overall market arrivals. This led to a slight supply-demand mismatch for CRC in December, further widening the price spread between HRC and CRC. Entering January, as automakers completed their year-end push for annual targets and export orders ended, coupled with the arrival of the Chinese New Year holiday, market trading activity gradually cooled, and the price spread between HRC and CRC subsequently narrowed.

II. The Price Spread Between HRC and CRC Will Continue to Fluctuate at High Levels in February-March

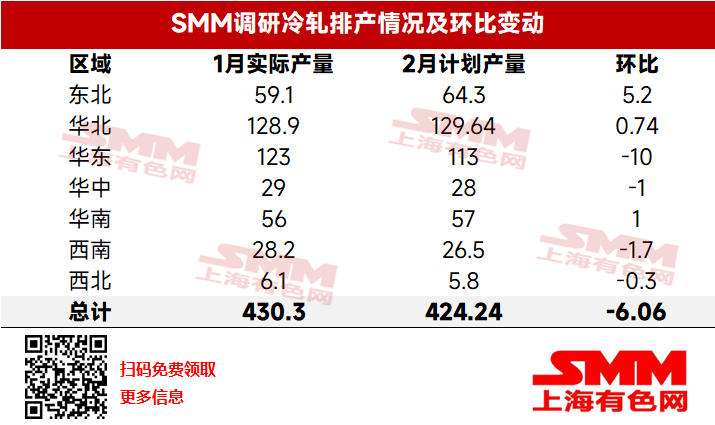

Looking ahead, in terms of CRC supply, according to the latest tracking by SMM, the planned production volume of CRC commercial materials by 31 mainstream steel mills in February totaled 4.2424 million mt, down 60,600 mt or 1.4% from the actual CRC commercial material production in January. On a daily average basis, February, with fewer days, had a planned daily average production of 151,500 mt, up 9.2% MoM from January's actual daily average production. Overall, CRC production in February is expected to remain at high levels. On the demand side, according to the latest report by ChinaIOL on the three major white goods, the total production schedule for air conditioners, refrigerators, and washing machines in February 2025 was 29.14 million units, up 30.6% YoY. By product, household air conditioner production was 15.93 million units, up 35.6% YoY; refrigerator production was 6.32 million units, up 29.2% YoY; and washing machine production was 6.89 million units, down 21.3% YoY. In January 2025, the operating rate of the automotive industry was 86.6%, up 6.9% YoY. However, the automotive industry weakened this month, as companies gradually suspended operations at month-end due to the Chinese New Year holiday, slowing production nationwide. Nevertheless, some companies reported continuing production during the holiday to meet backlog orders. SMM estimates the operating rate of the automotive industry in February to be around 83.6% and in March around 86.3%. Overall, downstream manufacturing is in a state of slow recovery.However, current CRC inventory in the market is not high. According to the latest data, total CRC inventory nationwide decreased by about 300,000 mt or 15% YoY based on the lunar calendar. In summary, the current supply-demand imbalance for CRC is not significant. During February-March, as the imbalance gradually accumulates, the price spread between HRC and CRC is expected to continue fluctuating at highs above 600 yuan/mt.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)